History

Crop Insurance: A History

Benjamin Franklin wrote, “I have sometimes thought it might be well to establish an office of insurance for farms against the damage that may occur to them from storms, blights, insects, etc.”

The first crop-hail insurance association is formed in Europe, where farmer demand for coverage was growing and early stock fire insurance companies first began to offer policies.

A group of tobacco farmers from Connecticut formed the first crop insurance company in America to insure against hail damage.

The first stock fire insurance company entered the business in America and offered hail insurance to a few prairie states, prompting more companies to follow.

More than a dozen stock fire insurance companies formed the Western Hail and Adjustment Association to devise a system for adjusting losses and compiling statistical data.

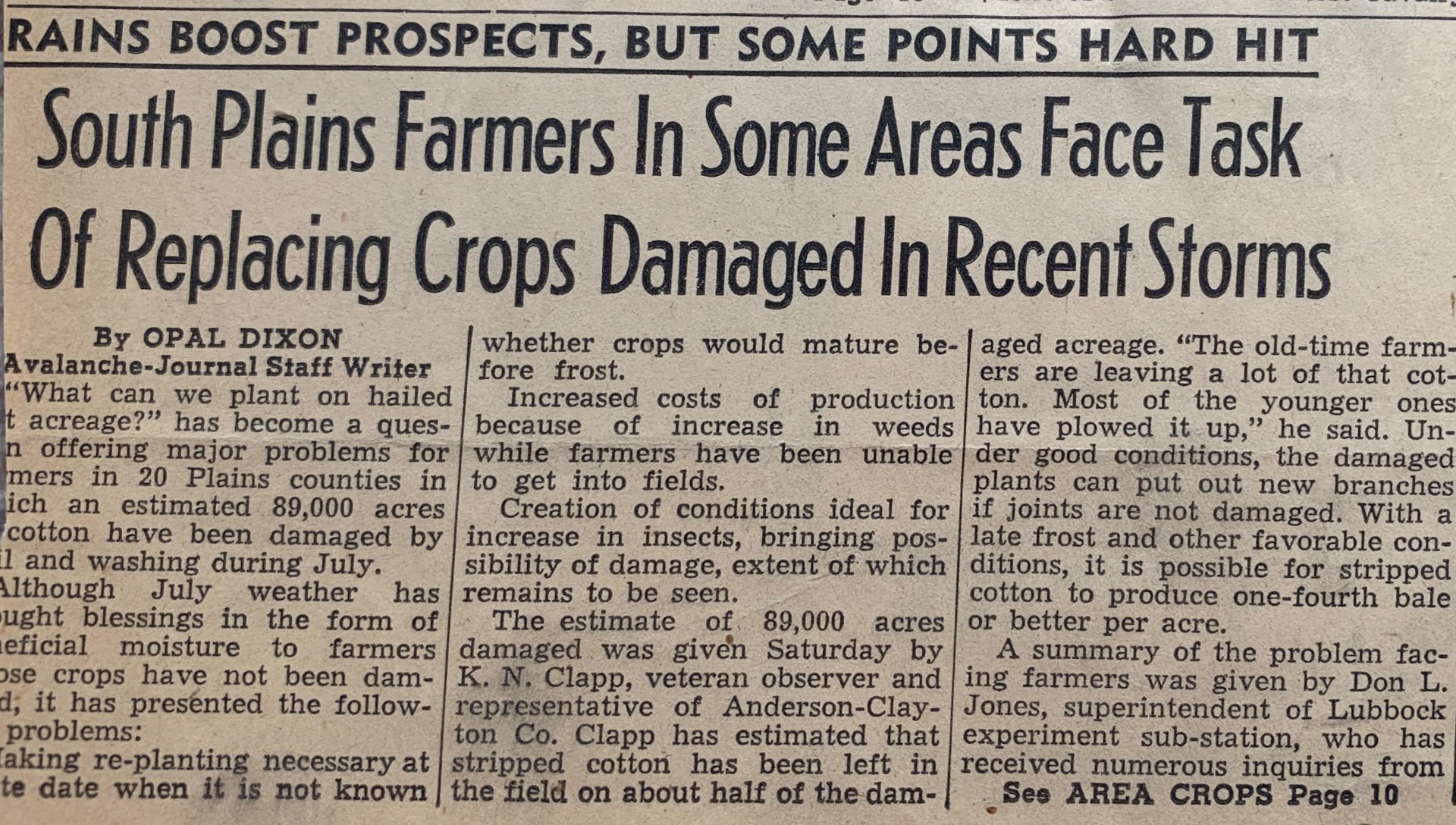

Hail insurance expanded and covered 25 percent of principal crop acreage in America, but farmers lacked coverage for perils beyond hail.

The Dust Bowl era began, killing crops and cattle, and showing how vulnerable U.S. agriculture was to non-hail disasters.

Congress passed the Federal Crop Insurance Act, which established the first multi-peril insurance program and created the Federal Crop Insurance Corporation to deliver coverage.

Low farmer participation led to the bankruptcy of the government’s Federal Crop Insurance Corporation.

The program was restructured on a limited experimental basis until 1979, but farmer participation remained very low in the government-delivered program.

Demand for private-sector hail insurance remained high and 62 companies formed the Crop-Hail Insurance Actuarial Association to advise companies on actuarial matters as the industry expanded.

Congress passed the Crop Insurance Act, allowing private-sector insurance delivery and establishing the public-private partnership that still exists today.

A major drought necessitated ad hoc disaster assistance as most farmers remained uninsured because coverage remained expensive and limited.

Bad weather necessitated another ad hoc disaster bill – the fourth in six years – prompting lawmakers to seek improvements to the crop insurance system.

Congress passed the Federal Crop Insurance Reform Act, which discounted premiums and established inexpensive catastrophic coverage to boost participation.

The USDA’s Risk Management Agency was formed to administer the FCIC and offer risk management and education programs to support U.S. agriculture.

Farmer participation skyrocketed with 180 million acres covered – more than triple the acres in 1988.

USDA defined Good Farming Practices (GFPs), encouraging farmers to adopt smart production practices, such as no-till planting. No-till is a way of planting crops without tilling the ground, improving carbon sequestration and soil health. According to the Conservation Technology Information Center (CTIC), no-till planting is now used on more than 65 million acres of farmland.

Congress passed the Agriculture Risk Protection Act, a bill that increased premium discounts, introduced revenue insurance, encouraged the private sector to create additional products, and targeted waste, fraud and abuse.

Crop insurance participation continued to climb, covering 210 million acres.

The crop insurance industry began a program to educate Indigenous farmers on their risk-management options, including crop insurance, supported by partial funding from RMA.

Crop insurers continued to improve coverage and expand product offerings, helping participation grow to 272 million acres.

Private-sector insurers entered into the current Standard Reinsurance Agreement with the government – a contract that spells out the business terms of Federal crop insurance.

The Farm Belt was hit with the worst drought since the Dust Bowl. Crop insurance paid $17 billion in indemnities and Congress did not need to pass supplemental disaster assistance.

The crop insurance industry began a partnership with the historically black 1890 Land-Grant Universities, offering free risk-management and business-planning workshops to socially disadvantaged and limited-resource farmers. Many of these workshops were supported by RMA and/or the National Institute of Food and Agriculture (NIFA) through competitive grants awarded to NCIS.

Congress passed the Agricultural Act, which strengthened crop insurance and positioned it as a cornerstone of farm policy.

The introduction of Whole-Farm Revenue Protection increased crop insurance accessibility and provided meaningful risk protection for non-traditional or specialty crops.

Congress passed the Agriculture Improvement Act, which built on the 2014 Farm Bill to expand product offerings, improve specialty crop coverage, and invest in beginning and veteran farmers.

Cover crops were recognized as a Good Farming Practice (GFP), giving farmers a new tool to help prioritize soil health and resiliency.

USDA released data that showed a record number of acres enrolled in crop insurance – nearly 400 million nationwide.

A new crop insurance plan, Hurricane Insurance Protection – Wind Index Endorsement, took effect just in time for the most active Atlantic hurricane season on record.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Crop Insurance: A Look Back

Because of the inherent risks and potential for widespread catastrophic losses associated with agricultural production, insuring farmers and ranchers has always posed a challenge.

Before the Federal Crop Insurance Program was established, private insurers had difficulty providing affordable insurance products to producers. In 1938, Congress passed the Federal Crop Insurance Act, which established the first Federal Crop Insurance Program. These early efforts were not particularly successful due to high program costs and low participation rates among farmers. The program had difficulty amassing sufficient reserves to pay claims and was not financially viable.

Congress recognized that other ways of assisting farmers through direct payments and disaster assistance needed to be created.

In 1980, Congress passed legislation to increase participation in the Federal Crop Insurance Program and make it more affordable and accessible. This modern era of crop insurance was marked by the introduction of a public-private partnership between the U.S. government and private insurance companies. Bringing the efficiencies of a private sector delivery system together with the regulatory and financial support of the federal government formed the basis of a new and innovative approach to solving a long-standing problem.

While the 1980 Act expanded the program by increasing the number of commodities insured, participation remained lower than Congress had hoped for. Members of Congress were growing weary of repeated requests for ad hoc disaster assistance and emergency loans that served to undermine the crop insurance program. Even as late as the early 1990’s, crop insurance participation rates hovered in the 30 percent range and Congress was often spending considerably more each year in disaster relief expenditures than it was on crop insurance.

The Federal Crop Insurance Reform Act of 1994 dramatically restructured the program. And in 1996, the Risk Management Agency (RMA) was created in the U.S. Department of Agriculture to administer the Federal Crop Insurance Program. Through subsidies built into the new program guidelines, participation increased dramatically. By 1998, more than 180 million acres of farmland were insured under the program, representing a three-fold increase over 1988.

In May of 2000, Congress approved another important piece of legislation: the Agricultural Risk Protection Act (ARPA). The provisions of ARPA made it easier for farmers to access different types of insurance products including revenue insurance and protection based on historical yields. ARPA also increased premium subsidy levels to farmers to encourage greater participation and included provisions designed to reduce fraud, waste and abuse.

The 2014 Farm Bill accelerated the evolution from traditional farm price and income support to risk management, solidifying crop insurance as the primary tool for farmers in dealing with production and price risk.

The 2008 Farm Bill’s direct and countercyclical payment programs and the state-based revenue program known as ACRE (Average Crop Revenue Enhancement Program) were eliminated. In their place, a farmer may choose one of two new farm programs that commenced with the 2014 crop year: 1) Price Loss Coverage (PLC), a program that makes a payment to a producer (at 85 percent of base acres) when the market price for a covered crop is below a fixed reference price; or 2) Agriculture Risk Protection (ARC), a program that makes a payment when either the farm’s revenue from all crops (ARC Individual) or the county’s revenue for a crop (ARC County) falls below 86 percent of a respective or benchmark-level of revenue. The maximum coverage band is 10 percentage points (76 percent to 86 percent of benchmark revenue). (ARC Individual pays at the 65 percent level while ARC County pays at 85 percent of base acres. The famer cannot have both.) ARC (either Individual or County) and PLC are designed to supplement crop insurance by providing support in periods of multi-year price declines and helping producers cover the crop insurance policy’s deductible. Both ARC and PLC are subject to payment limits. Together these two farm programs are projected over time to spend substantially less than the programs they replaced.

In addition to these two new farm programs, the 2014 Farm Bill strengthened crop insurance by adding several new products and requiring a number of program revisions to increase crop insurance’s role as the primary component of the farm safety net. The major enhancement to crop insurance is the addition of two supplemental policies that will help producers expand their protection against losses due to natural disasters or price declines.

The first program, the Stacked Income Protection Plan, or STAX, is for upland cotton acreage only, as cotton producers are not eligible for ARC or PLC. STAX is an area revenue plan that a cotton producer may use alone or in combination with an underlying policy or plan of insurance. STAX is similar in design to the existing area plan called Area Revenue Protection (ARP) can be chosen as a stand-alone policy or in combination with an individual or area plan of insurance. STAX is available in all counties where Federal crop insurance coverage is available for upland cotton. It is also available by practice, irrigated or non-irrigated. STAX covers revenue losses of not less than 10 percent and not more than 30 percent of expected county revenue. An indemnity is paid based on the amount that expected county revenue exceeds actual county revenue. Producers receive a premium discount equal to 80 percent of the STAX premium, and on behalf of the producer, an administrative and operating expense payment is made to the crop insurance companies to compensate for a portion of delivery expenses.

The second program, the Supplemental Coverage Option, or SCO, provides certain crop producers with the option to purchase area coverage in combination with an underlying individual policy or plan of insurance that would allow indemnities to be equal to a part of the deductible on the underlying individual plan of insurance. SCO indemnities are triggered if area losses exceed 14 percent of expected levels, with SCO coverage not to exceed the difference between 86 percent and the coverage level selected by the producer for the underlying policy. SCO coverage is not available for crops enrolled in ARC or acreage that is enrolled in STAX. Producers receive a premium discount equal to 65 percent of the SCO premium, and on behalf of the producer, an administrative and operating expense payment is made to the crop insurance companies to compensate for a portion of delivery expenses.

The Agricultural Improvement Act of 2018, commonly referred to as the 2018 Farm Bill, strengthened crop insurance by adding new products and directing research to the development of products for additional crops and modifying existing programs to address non-traditional agricultural commodities and/or production and marketing systems and issues related to catastrophic crop losses. These actions will increase crop insurance’s role as a key component of the farm safety net. In addition, the bill makes a number of changes to the details of individual parts of the crop insurance system with a view to improving the delivery and management system and working more closely with other allied USDA agencies.

Among the new programs is the addition of hemp to the list of commodities that will be eligible for insurance. Direction for research includes the development of polices to insure the production of or revenue derived from the production of hops, the production of products targeted to local consumers and markets, new and innovative irrigation practices for rice and improvements in existing citrus fruit policies.

The bill places an emphasis on the development of continued growth in the Whole Farm Revenue Polices (WFRP). Specifically, the bill directs RMA to take steps necessary to streamline, add flexibility or tailor program rules to make WFRP provide meaningful risk protection for non-traditional agricultural commodities (e.g. aquaculture) or production and marketing systems (e.g. urban, local food, or greenhouses), that are not served as well under current yield or revenue-based policies for individual crops.

The bill also directs FCIC to carry out research on the development of polices that would address low frequency, catastrophic losses due to weather events such as tropical storms or hurricanes. Such policies would address production and/or revenue losses. These policies would be designed to address situations such as the storm damage to crops in 2017 and 2018 where high levels of participation at low levels of coverage resulted in passage of additional ad hoc disaster assistance.

Because of the inherent risks and potential for widespread catastrophic losses associated with agricultural production, insuring farmers and ranchers has always posed a challenge.

Early 20th Century

Before the Federal Crop Insurance Program was established, private insurers had difficulty providing affordable insurance products to producers. In 1938, Congress passed the Federal Crop Insurance Act, which established the first Federal Crop Insurance Program. These early efforts were not particularly successful due to high program costs and low participation rates among farmers. The program had difficulty amassing sufficient reserves to pay claims and was not financially viable.

Congress recognized that other ways of assisting farmers through direct payments and disaster assistance needed to be created.

Federal Crop Insurance Act of 1980

In 1980, Congress passed legislation to increase participation in the Federal Crop Insurance Program and make it more affordable and accessible. This modern era of crop insurance was marked by the introduction of a public-private partnership between the U.S. government and private insurance companies. Bringing the efficiencies of a private sector delivery system together with the regulatory and financial support of the federal government formed the basis of a new and innovative approach to solving a long-standing problem.

While the 1980 Act expanded the program by increasing the number of commodities insured, participation remained lower than Congress had hoped for. Members of Congress were growing weary of repeated requests for ad hoc disaster assistance and emergency loans that served to undermine the crop insurance program. Even as late as the early 1990’s, crop insurance participation rates hovered in the 30 percent range and Congress was often spending considerably more each year in disaster relief expenditures than it was on crop insurance.

The Federal Crop Insurance Reform Act of 1994 and the Creation of the Risk Management Agency

The Federal Crop Insurance Reform Act of 1994 dramatically restructured the program. And in 1996, the Risk Management Agency (RMA) was created in the U.S. Department of Agriculture to administer the Federal Crop Insurance Program. Through subsidies built into the new program guidelines, participation increased dramatically. By 1998, more than 180 million acres of farmland were insured under the program, representing a three-fold increase over 1988.

The Agricultural Risk Protection Act (ARPA)

In May of 2000, Congress approved another important piece of legislation: the Agricultural Risk Protection Act (ARPA). The provisions of ARPA made it easier for farmers to access different types of insurance products including revenue insurance and protection based on historical yields. ARPA also increased premium subsidy levels to farmers to encourage greater participation and included provisions designed to reduce fraud, waste and abuse.

2014 Farm Bill

The 2014 Farm Bill accelerated the evolution from traditional farm price and income support to risk management, solidifying crop insurance as the primary tool for farmers in dealing with production and price risk.

The 2008 Farm Bill’s direct and countercyclical payment programs and the state-based revenue program known as ACRE (Average Crop Revenue Enhancement Program) were eliminated. In their place, a farmer may choose one of two new farm programs that commenced with the 2014 crop year: 1) Price Loss Coverage (PLC), a program that makes a payment to a producer (at 85 percent of base acres) when the market price for a covered crop is below a fixed reference price; or 2) Agriculture Risk Protection (ARC), a program that makes a payment when either the farm’s revenue from all crops (ARC Individual) or the county’s revenue for a crop (ARC County) falls below 86 percent of a respective or benchmark-level of revenue. The maximum coverage band is 10 percentage points (76 percent to 86 percent of benchmark revenue). (ARC Individual pays at the 65 percent level while ARC County pays at 85 percent of base acres. The famer cannot have both.) ARC (either Individual or County) and PLC are designed to supplement crop insurance by providing support in periods of multi-year price declines and helping producers cover the crop insurance policy’s deductible. Both ARC and PLC are subject to payment limits. Together these two farm programs are projected over time to spend substantially less than the programs they replaced.

In addition to these two new farm programs, the 2014 Farm Bill strengthened crop insurance by adding several new products and requiring a number of program revisions to increase crop insurance’s role as the primary component of the farm safety net. The major enhancement to crop insurance is the addition of two supplemental policies that will help producers expand their protection against losses due to natural disasters or price declines.

The first program, the Stacked Income Protection Plan, or STAX, is for upland cotton acreage only, as cotton producers are not eligible for ARC or PLC. STAX is an area revenue plan that a cotton producer may use alone or in combination with an underlying policy or plan of insurance. STAX is similar in design to the existing area plan called Area Revenue Protection (ARP) can be chosen as a stand-alone policy or in combination with an individual or area plan of insurance. STAX is available in all counties where Federal crop insurance coverage is available for upland cotton. It is also available by practice, irrigated or non-irrigated. STAX covers revenue losses of not less than 10 percent and not more than 30 percent of expected county revenue. An indemnity is paid based on the amount that expected county revenue exceeds actual county revenue. Producers receive a premium discount equal to 80 percent of the STAX premium, and on behalf of the producer, an administrative and operating expense payment is made to the crop insurance companies to compensate for a portion of delivery expenses.

The second program, the Supplemental Coverage Option, or SCO, provides certain crop producers with the option to purchase area coverage in combination with an underlying individual policy or plan of insurance that would allow indemnities to be equal to a part of the deductible on the underlying individual plan of insurance. SCO indemnities are triggered if area losses exceed 14 percent of expected levels, with SCO coverage not to exceed the difference between 86 percent and the coverage level selected by the producer for the underlying policy. SCO coverage is not available for crops enrolled in ARC or acreage that is enrolled in STAX. Producers receive a premium discount equal to 65 percent of the SCO premium, and on behalf of the producer, an administrative and operating expense payment is made to the crop insurance companies to compensate for a portion of delivery expenses.

2018 Farm Bill

The Agricultural Improvement Act of 2018, commonly referred to as the 2018 Farm Bill, strengthened crop insurance by adding new products and directing research to the development of products for additional crops and modifying existing programs to address non-traditional agricultural commodities and/or production and marketing systems and issues related to catastrophic crop losses. These actions will increase crop insurance’s role as a key component of the farm safety net. In addition, the bill makes a number of changes to the details of individual parts of the crop insurance system with a view to improving the delivery and management system and working more closely with other allied USDA agencies.

Among the new programs is the addition of hemp to the list of commodities that will be eligible for insurance. Direction for research includes the development of polices to insure the production of or revenue derived from the production of hops, the production of products targeted to local consumers and markets, new and innovative irrigation practices for rice and improvements in existing citrus fruit policies.

The bill places an emphasis on the development of continued growth in the Whole Farm Revenue Polices (WFRP). Specifically, the bill directs RMA to take steps necessary to streamline, add flexibility or tailor program rules to make WFRP provide meaningful risk protection for non-traditional agricultural commodities (e.g. aquaculture) or production and marketing systems (e.g. urban, local food, or greenhouses), that are not served as well under current yield or revenue-based policies for individual crops.

The bill also directs FCIC to carry out research on the development of polices that would address low frequency, catastrophic losses due to weather events such as tropical storms or hurricanes. Such policies would address production and/or revenue losses. These policies would be designed to address situations such as the storm damage to crops in 2017 and 2018 where high levels of participation at low levels of coverage resulted in passage of additional ad hoc disaster assistance.